Anthropic at 92%: Three Surfaces Tell the Same Story

Polymarket, Ramp, and GitHub trending all price Anthropic dominance. Where they agree, where they disagree, what operators should do.

Three independent telemetry surfaces just rhymed.

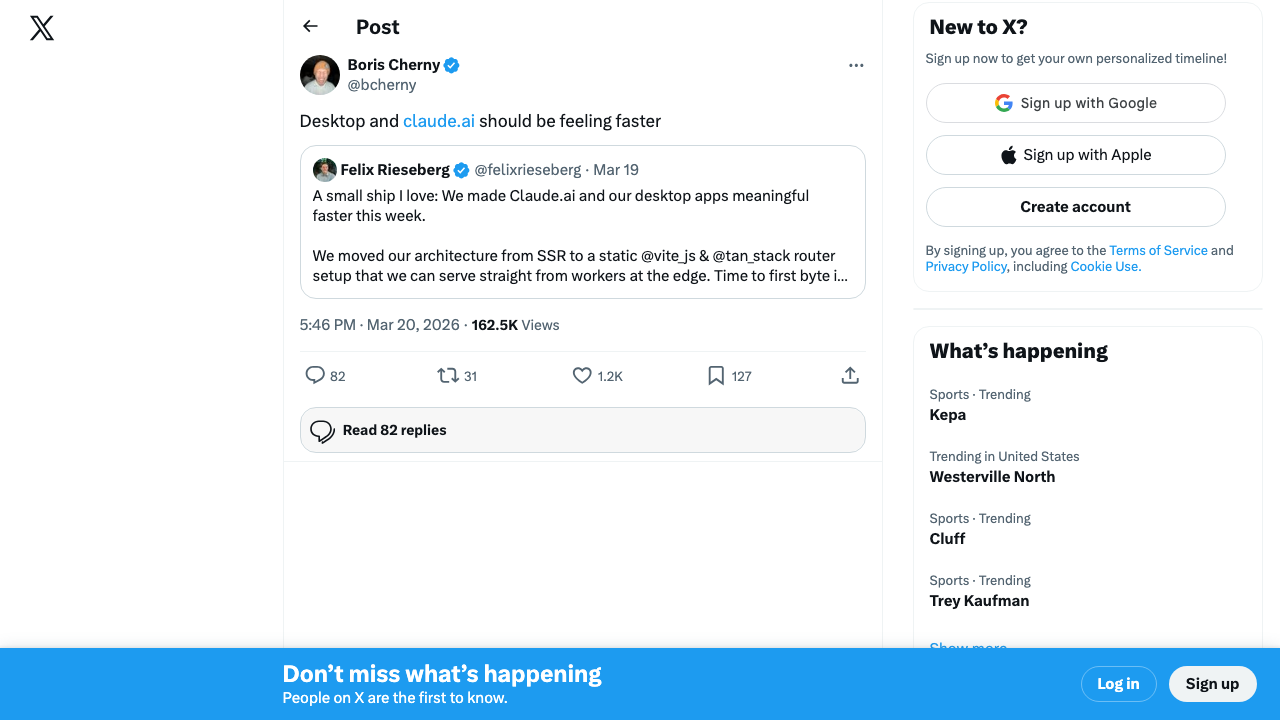

Polymarket's "Which company has the best AI model end of May" sits at Anthropic 92%, Google 6%, OpenAI 1% — on $428,985 of 24-hour volume and $2.4M of liquidity, the deepest book in the AI-market category. Boris Cherny's Ramp AI Index post showed Anthropic at 34.4% of enterprise card spend versus OpenAI at 32.3%, with Anthropic's adoption up roughly 4× year-over-year while OpenAI sat flat at +0.3%. And on the developer surface, four of the top eleven repos on GitHub trending today are explicitly Claude-Code-skills-shaped — the fourth consecutive day of the same compositional pattern.

Three surfaces. One name. The interesting question is not whether Anthropic is winning — every telemetry surface we can read agrees that it is. The interesting question is what each surface is actually measuring, where the three disagree, and what an operator should do with the disagreement.

The triangulation play. When prediction-market price, enterprise-spend share, and developer-mindshare all move together, you have something rare in markets: three independent observers pricing the same outcome through different cost functions. The signal isn't the agreement. It's the disagreement points — that's where there's still alpha.

1. The Polymarket leg — what's priced, what's not

The headline market — which-company-has-the-best-ai-model-end-of-may — prices Anthropic at 92% with thirteen days left in the month. With $2.4M of liquidity sitting on the book, this is not a thin Polymarket curiosity. It is the deepest AI-leaderboard market currently trading.

Three things to notice before reading this as "Anthropic won."

First, the Style Control On variant — same question, but normalized for response-length and formatting effects on LMSYS Arena — sits at 93% but has moved down 17% this month. The market is less convinced of Anthropic dominance under style-controlled conditions than under raw conditions. That gap is the leaderboard's response-length bias being priced in real time.

Second, when you shift the horizon to year-end, the picture inverts. The market which-companies-will-have-a-1-ai-model-by-december-31 — which companies will hold #1 at any point through end-of-year — prices Google at 72%, OpenAI at 41%, and xAI at 20%. Anthropic does not break the top three on the multi-month horizon. The market believes Anthropic owns right now but expects the lead to rotate before year-end. That's a strong claim and a tradeable one.

Third, June already prices differently. Anthropic drops from end-of-May 92% to end-of-June 74% on the equivalent market. The market expects a release cadence from one or more of (Google Gemini 3.5, OpenAI GPT-5.5 successor, xAI Grok) that closes some of the gap inside thirty days. If you are making a vendor decision based on the 92%, you are making a six-week decision, not a twelve-month decision.

2. The Ramp leg — what card-spend telemetry actually proxies for

Ramp is a corporate card platform. The Ramp AI Index reports the share of card-spend on AI vendor categories across its customer base. Boris Cherny's post — Anthropic engineer — flagged the latest cut: Anthropic 34.4% of AI card-spend, OpenAI 32.3%, with Anthropic's curve up roughly 4× YoY while OpenAI's curve has gone effectively flat at +0.3%.

The Ramp data is the most-cited and the most-misread of the three legs. Three things it is not:

It is not usage. Card-spend tells you who is paying. It does not tell you how many tokens, how many users, or how many seats are deployed. A company that buys $50K of Claude credits via corporate card and a company that buys $50K of ChatGPT Enterprise via the same card look identical to Ramp. Whether one is being aggressively rolled out and the other shelved is invisible.

It is not market share. Ramp's customer base is a specific cut of US-based, post-Series-A SaaS-and-fintech companies. Enterprise contracts that flow through procurement and AP, not corporate cards, are entirely outside the dataset. The big-ticket OpenAI enterprise deals (Microsoft-routed, custom-billed) are precisely the kind of transactions that do not appear here.

The YoY ratio is real. Even with the caveats, the 4× year-over-year vs. +0.3% comparison is striking. It is consistent with the story that Claude has become the new-budget AI vendor across the Ramp customer cohort — the line item that mid-market companies added in the last twelve months. OpenAI's flat curve is not a decline; it is a saturation pattern. The companies who were going to use OpenAI a year ago still are. The new companies are buying Anthropic.

The right way to read Ramp is as a leading indicator for SaaS-and-fintech-startup adoption, not a definitive market-share figure. It rhymes with the API-developer-platform story we covered — the developer surface is where Anthropic is winning incremental dollar, and Ramp is the cleanest telemetry for that surface.

3. The GitHub mindshare leg — category consolidation

The third surface is the noisiest and the most interesting.

For four consecutive days, GitHub trending has been dominated by repos with a Claude-Code-skills shape. Today's cut: Imbad0202/academic-research-skills at ★1,302, tech-leads-club/agent-skills at ★1,244, rohitg00/agentmemory at ★1,226, and K-Dense-AI/scientific-agent-skills at ★610. Yesterday it was Karpathy's CLAUDE.md template and Composio's skills bundle. The day before, mattpocock's directory race and the openhuman runaway #1.

Four days of the same composition is not a meme — it is a category consolidating. The repos are converging on three archetypes:

- Skills registries — curated bundles of

.mdfiles describing capabilities a Claude Code instance can pull in at runtime. Academic-research-skills, agent-skills, scientific-agent-skills, the obra superpowers framework variant — all share the same directory layout, the sameSKILL.mdfrontmatter, the same Anthropic-published Skills spec underneath. - Agent memory — persistent context layers that survive across sessions. agentmemory's ★1,226 day-one is the signal that "long-running" has become an explicit engineering category, not a prompting trick.

- Agent toolkits — earendil-works/pi, CLI-Anything, microsoft/ai-agents-for-beginners. The framing is "make every CLI agent-native" — explicitly framed against the Claude Code substrate as the reference target.

What makes this a mindshare signal rather than a usage signal: GitHub stars don't pay rent. The developers chasing these repos are not paying Anthropic. But they are choosing what to read, what to fork, what to publish on top of — and the substrate they are publishing on top of is Claude Code. That's how categories form. Not when one vendor wins the spend; when the publishing surface tilts toward one vendor's substrate as the default to extend.

4. Where the three surfaces disagree

The three telemetry surfaces agree on direction. The interesting question is where they diverge.

Disagreement #1: Time horizon. Polymarket is bullish at four weeks and bearish at eight months — the multi-month horizon prices Google at 72% to hold #1 at some point in the year. Ramp is structurally a six-month indicator (card-spend rebases slowly). GitHub mindshare is a four-week indicator (categories consolidate fast and rotate faster). If you trust all three, you should trust Anthropic dominance for the next thirty days, hedge for a Q3/Q4 rotation, and assume the GitHub-trending composition will look completely different by August.

Disagreement #2: What "win" means. Polymarket prices model-leaderboard wins. Ramp prices spend share. GitHub prices substrate share. These are three different products. It is possible — and historically common — for one vendor to own model-leaderboard while another owns spend share while a third owns substrate. The current pattern of all three pointing the same way is the unusual case. The more common case is fragmentation. If the disagreement starts opening, watch the substrate leg — substrate share is the stickiest of the three.

Disagreement #3: Who's actually using the product. Ramp says SaaS-and-fintech mid-market. GitHub mindshare says developers and AI-tooling builders. Polymarket prices a leaderboard that LMSYS Arena visitors curate. None of these three populations is "enterprise IT buyer at a Fortune 500." The biggest blind spot in the triple-leg is the procurement-driven enterprise segment that flows through neither cards, nor GitHub, nor LMSYS — and where OpenAI's Microsoft channel is still the dominant lane.

5. The Stainless acquihire — Anthropic builds the platform layer

The under-reported story today is the Anthropic acquires Stainless news that hit HN front-page at ★70 with thirty-four comments. Stainless is an SDK-generator company — it produces typed SDKs from OpenAPI specs for the kind of companies that ship developer platforms.

The HN comment thread is reading this as an acquihire and the hosted Stainless product is being wound down. That's not the interesting framing.

The interesting framing is what Anthropic is signaling about its own product roadmap. If you're acquiring an SDK-generation team, you're not optimizing for prompt engineering. You're optimizing for an agent API — the kind of platform surface where third-party developers publish skills, sub-agents, and integrations and Anthropic ships them typed bindings across five languages.

Combine that with this week's other signals:

- The Build Agents That Run for Hours Anthropic talk laying out adversarial-evaluator + structured-handoff patterns

- The ADLC framing from AI LABS — "Agent Development Lifecycle" as a successor to vibe coding

- The Peter Yang Anthropic interview where Anthropic says "we treat the model like a product, but model development is growing, not speccing"

- The Karpathy CLAUDE.md template going viral with hundreds of repos shipping the convention

The composition is clear. Anthropic is no longer just a model vendor. It is building the platform layer — the runtime, the skills convention, the SDK pipeline, the agent lifecycle. The Stainless acquihire is the SDK piece of the puzzle.

The HN comment thread on today's Stainless news lands on a similar read — the wind-down of the hosted Stainless generator is being framed not as a product failure but as a transparent acquihire-for-capability play, with the SDK pipeline migrating into Anthropic's own developer surface. That is the platform-build signal in plain sight.

For operators. Three months ago the question was "should we use Claude or GPT?" Today the question is closer to "should we build on top of Claude Code's runtime, or roll our own?" That is a different question with a different answer. If Anthropic continues consolidating the substrate layer, the build-vs-buy line on agent runtimes is going to shift fast. The "we'll do it ourselves on top of an OpenAI-compatible interface" answer that worked in 2024 doesn't hold up against a Claude Code platform that publishes typed SDKs, ships skills, and has four consecutive days of trending repos extending it.

What an operator should do this week

Three concrete actions:

1. Re-time your vendor review. If you locked a six-month contract this quarter on the assumption that the model leader was stable, the Polymarket end-of-June pricing (Anthropic 74% vs end-of-May 92%) says you should re-time your review window. The market believes the lead is contestable within thirty days. Bake quarterly review checkpoints in.

2. Read your own Ramp. If your finance team uses Ramp or Brex, pull your last six months of AI-vendor card spend. The Ramp aggregate masks enormous variance — your specific cohort may be 70/30 Claude or 70/30 OpenAI. The aggregate gives you the macro; your own cut gives you the action. The Anthropic-vs-OpenAI overtake story shows up in customer data well before it shows up in aggregate filings.

3. Watch the substrate layer. Don't optimize your stack for the model leaderboard — optimize it for the substrate. If the GitHub trending pattern persists another two weeks, the answer is to invest in skill authorship and runtime instrumentation on the Claude Code substrate, regardless of which model leads next quarter. The substrate is the durable bet; the leaderboard is the trade.

The 92% number is loud. The disagreement points are louder. The story under the story is the platform pivot — and that is the thing that lasts past June 30.

Originally published at ComputeLeap.

About ComputeLeap Team

The ComputeLeap editorial team covers AI tools, agents, and products — helping readers discover and use artificial intelligence to work smarter.

💬 Join the Discussion

Have thoughts on this article? Discuss it on your favorite platform:

Related Articles

Anthropic's S-1: What a $965B IPO Filing Changes

Anthropic filed its S-1 after a $65B Series H. What the confidential filing reveals about timing, AI capital risk, and the bull case.

Karpathy Joins Anthropic — and Polymarket Priced It at 74%

Karpathy + Jensen's multi-cloud Anthropic capacity + Polymarket at 74% are one story: AI labor, compute, and conviction repriced in the same week.

Per-Seat SaaS Is a Liability: A 2026 Operator's Checklist

Palantir says SaaS is dead, Benioff calls it the third SaaSpocalypse, and HN is pricing the time bomb. Three failure modes and a buyer's checklist.

The ComputeLeap Weekly

Get a weekly digest of the best AI infra writing — Claude Code, agent frameworks, deployment patterns. No fluff.

Weekly. Unsubscribe anytime.